The Federal Reserve (Fed) completed its third scheduled policy meeting of the year Wednesday, June 10, and continued to signal strong support for the economy, committing to keeping rates near zero until it is confident of a recovery and maintaining bond purchases (“quantitative easing”), at least at the current level.

“Despite some early signs of economic improvement, the Fed reinforced that it will remain supportive until uncertainty lifts and the economy is in a stable, sustained recovery, and that may mean no rate hikes until 2023,” said LPL Financial Senior Market Strategist Ryan Detrick.

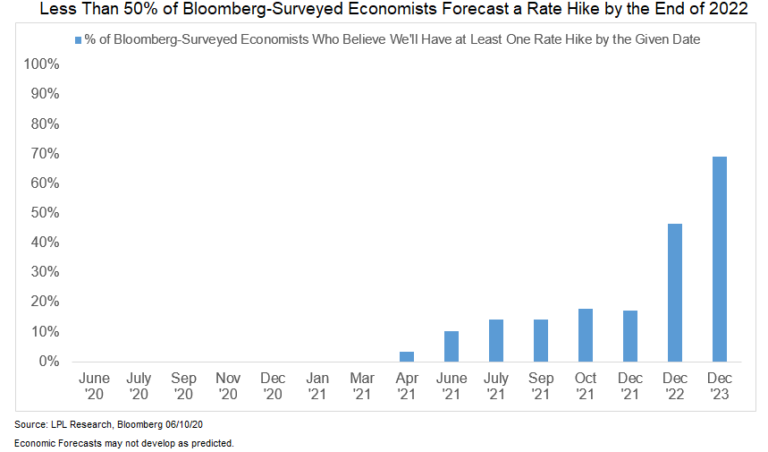

In fact, in its first set of forecasts since December 2019, 15 of 17 Fed policy committee participants did not see a rate hike until 2023 at the earliest. As shown in the LPL Chart of the Day, economists surveyed by Bloomberg were only somewhat more upbeat, with less than 50% forecasting a rate hike as early as 2022.

In his press conference following the conclusion of the meeting, Fed Chair Jerome Powell emphasized that the course of the downturn and recovery remains “extraordinarily uncertain.” In the face of that uncertainty, we believe the Fed will be extremely cautious about acting prematurely. He also discussed added measures the Fed is looking at to further reassure markets and support the economy, such as more specific forward guidance on the conditions under which it would consider raising rates and “yield curve control,” a process in which the Fed purchases enough bonds to place a cap on short to intermediate Treasury yields, possibly out to maturities as long as five years.

While we believe economic improvement is likely to push rates higher at longer maturities over the rest of 2020, forward guidance and yield curve control should help keep shorter maturities well anchored, which may limit movement at the longer end. Our baseline forecast remains that the 10-year Treasury yield could push out over 1.25% by the end of 2020, but we see only a limited chance of a significant move that would push the 10-year all the way back toward 2%.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. All market and index data comes from Factset and Marketwatch.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Yield Curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality, but differing maturity dates. The most frequently reported yield curve compares the three-month, two-year, five-year and 30-year U.S. Treasury debt. This yield curve is used as a benchmark for other debt in the market, such as mortgage rates or bank lending rates. The curve is also used to predict changes in economic output and growth.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value