As you near age 65, you may start to think about Medicare. How do you sort through your coverage options? When (and how) do you enroll? And what if you have other health insurance? Here is some information to help you when it’s time to make decisions about Medicare.

Medicare coverage basics

Medicare, the federal health insurance program that covers most people who are 65 and older, is made up of different parts that help cover specific services.

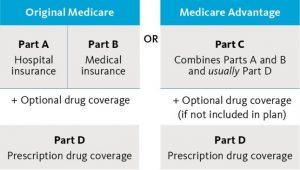

Original Medicare is divided into hospital insurance (Part A) and medical insurance (Part B), which are run by the federal government. Medicare Part C (Medicare Advantage) and Part D (prescription drug coverage) are provided by private insurance companies approved by Medicare.

Medicare Part A (hospital insurance)

Part A covers services associated with inpatient care in a hospital, skilled nursing facility, or psychiatric hospital. It covers charges for the room, meals, and nursing services. Part A also covers hospice care and home health care, but not long-term care. Part A is premium-free for most people, but deductibles and coinsurance costs apply to some services.

Medicare Part B (medical insurance)

Part B covers other medical care, including inpatient or outpatient physician care, lab tests, physical therapy, and ambulance services. Medicare Part B also covers 100% of the cost of many preventive services. Everyone pays a monthly premium for Part B. Most people pay the standard monthly premium, which is $170.10 in 2022. People with higher incomes may pay more than this amount, while some people will pay less. Beneficiaries will need to meet an annual deductible and after that pay 20% of the Medicare-approved amount for most services.

Medicare Part C (Medicare Advantage)

A Medicare Advantage plan is a private, all-in-one health-care plan that contracts with Medicare to provide Part A and Part B benefits. A Medicare Advantage plan covers all of the services that Original Medicare covers. Some plans offer extra coverage for expenses not covered by Original Medicare such as vision, hearing, and dental costs. Most also offer prescription drug (Part D) coverage. Several types of Medicare Advantage plans may be available, including HMOs and PPOs. There is a separate monthly premium for the Medicare Advantage plan in addition to the monthly Part B premium.

Medicare Part D (prescription drug coverage)

All Medicare beneficiaries are eligible to join a Medicare prescription drug plan offered by private companies or insurers that have been approved by Medicare. Premiums, copayments, and coinsurance costs vary by plan, but all cover a broad number of brand-name and generic drugs.

Choosing a Medicare plan

When it’s time to enroll in Medicare, you can choose how you want to get your coverage. There are two main ways, as shown in the chart below.

If you decide to enroll in Original Medicare, you may also want to consider purchasing Medicare Supplement Insurance (Medigap). Sold by private insurers, Medigap policies are designed to help cover Original Medicare’s deductibles, copayments, and coinsurance costs. If you have a Medicare Advantage plan, you don’t need (and can’t enroll in) Medigap.

When choosing coverage, compare the costs and benefits. Here are a few things to consider.

| Original Medicare | Medicare Advantage |

| You can go to any doctor who accepts Medicare, and in most cases don’t need referrals to see specialists | You’ll generally need to use a doctor in the plan’s network and may need referrals to see specialists |

| There’s no limit on out-of-pocket costs | Plans have a yearly limit on out-of-pocket costs |

| You pay a monthly premium for Part B | You pay a monthly premium for the plan and a monthly premium for Part B, but some plans have a zero premium or will pay all or part of your Part B premium |

| You pay extra for Part D prescription drug coverage | Most plans include Part D prescription drug coverage |

When and how to enroll

If you’ve been receiving Social Security or Railroad Retirement Board benefits for at least four months before you turn 65, you will be enrolled automatically in Original Medicare Parts A and B. The Social Security Administration will notify you that you’ve been enrolled, and you’ll get your Medicare card in the mail three months before your 65th birthday.*

If you are not already receiving Social Security or Railroad Retirement Board benefits and want to sign up for Medicare, you’ll need to apply online, by phone, or by visiting your local Social Security office.

Your initial enrollment period starts three months before the month you turn 65 and ends three months after the month you turn 65. The start date of your coverage depends on when you enroll.

If you have been automatically enrolled but decide to decline coverage or do not enroll in Medicare Part B during the initial enrollment period, you can enroll later during the annual general enrollment period that runs from January 1 to March 31 each year, with coverage beginning on July 31. However, late-enrollment penalties may apply in some situations.

What if you already have health insurance through an employer?

You can generally wait to enroll in Medicare past age 65 if you have group health insurance through your employer or your spouse’s employer. Most employers can’t require employees or covered spouses to enroll in Medicare to retain eligibility for their group health benefits. However, some small employers can, so contact your plan’s benefits administrator to find out if you’re required to sign up for Medicare when you reach age 65 and how your group health coverage works with Medicare.

If you have Medicare and group health coverage, both insurers may cover your medical costs, based on “coordination of benefit” rules. The primary insurer pays your claim first, up to the limits of the policy. The secondary insurer pays your claim only if there are costs the primary insurer didn’t cover, but all uncovered costs may not be paid.

Because Medicare Part A is free for most people, consider enrolling in Part A even if you have employer coverage to help fill any coverage gaps. Medicare Part B requires premium payments, so compare the costs and benefits to your employer’s plan.

If you didn’t sign up for Medicare when you were first eligible because you had group health coverage through an employer, late-enrollment penalties generally do not apply. You can sign up for Medicare Part A and/or Part B at any time as long as you are covered by a group health plan through your own employer or your spouse’s employer. If you stop working or your coverage ends, you will have an eight-month period to sign up without penalty.

What if you don’t like the coverage you’ve chosen?

You can make coverage changes at certain times during the year. From October 15 through December 7, you can join, switch, or drop a Medicare health or drug plan for the following year. You may also be able to make changes during special enrollment periods. For example, if you enrolled in a Medicare Advantage plan during your initial enrollment period, you can switch to an Original Medicare plan at any time during the 12-month period that begins on your effective date of coverage or make coverage changes every year from January 1 through March 31 (the Medicare Advantage open enrollment period).

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The information provided is not intended to be a substitute for specific individualized tax planning or legal advice. We suggest that you consult with a qualified tax or legal professional.

LPL Financial Representatives offer access to Trust Services through The Private Trust Company N.A., an affiliate of LPL Financial.

This article was prepared by Broadridge.

LPL Tracking #1-05094044