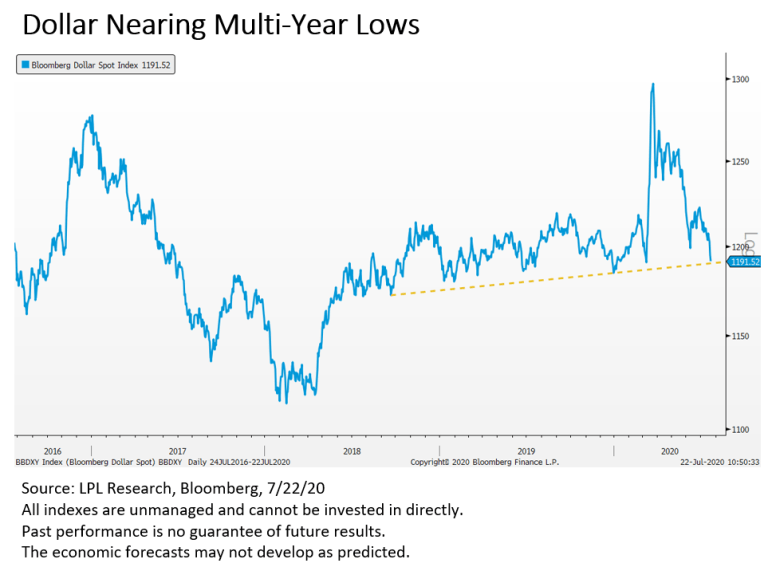

The US dollar was remarkably strong during the first quarter of 2020, benefitting from the flight to safety and rallying to nearly a 10% year-to-date gain at the stock market’s low point on March 23. However, as equity markets have recovered, and the US has continued to fight the COVID-19 pandemic, the dollar has given up nearly all of those gains. We think this trend may continue, and if so, it would have important implications for a range of asset classes.

As shown in the LPL Chart of the Day, the Bloomberg Dollar Spot Index, a more diversified basket than the commonly cited DXY Index, is nearing a critical uptrend line. A break of this support could mean that weakness seen over the past few months is more than just an unwinding of the flight to safety. Through Wednesday, the index was down more than 1% for the week and tracking toward its fourth straight weekly loss.

This isn’t just a technical story though. As we explored last month, rising twin deficits have historically been followed by a weaker dollar, meaning the fundamentals support this move as well.

The commodity rally is another reason to believe the market may be looking toward a weaker dollar. Commodities are typically viewed as having an inverse relationship with the dollar since the dollar is effectively the denominator of a hard asset. Gold prices are up more than 20% year to date, copper just traded to its highest level in more than two years, and silver prices have appreciated 28% this month alone.

As for the implications of a weaker dollar, according to LPL Chief Market Strategist Ryan Detrick, “a weaker US dollar may be a slight negative for US consumers’ buying power, but for investors’ portfolios the implications are overwhelmingly positive. Commodities are rallying, US multinational companies benefit from foreign buyers being able to afford more of their goods, and international stocks do well as their underlying currencies appreciate.”

Recent history bears this out. The last calendar year that saw a significant dollar decline was 2017 when the Bloomberg Dollar Index fell more than 8%. The S&P 500 Index rallied more than 19% on a price return basis; however, international stocks fared even better. The MSCI EAFE Index and MSCI Emerging Markets Index gained 22% and 34%, respectively, and 2017 represented the only year since 2012 that either outperformed the US.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from Factset and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

{kind=link}