Market Blog

Fixed-income investors aren’t used to having to deal with the volatility of stocks, but in the year that is 2020, that is exactly what has happened thus far. Unfortunately, while we don’t see the volatility of Q1 2020 continuing in 2021, we do believe that interest rates may continue to rise in 2021, and this may put more near-term pressure on bond returns.

Two technical reasons lead us to believe that the yield on the 10-year Treasury note has not only bottomed but could be headed higher in 2021.

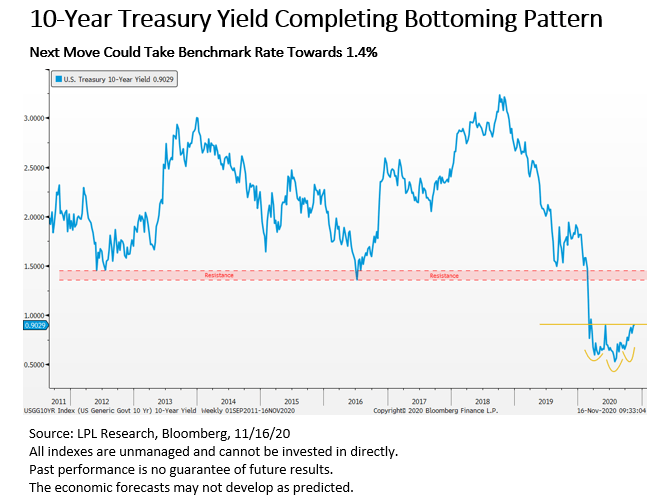

Inverse Head and Shoulders Pattern

One of the most well-known patterns in technical analysis is the Head and Shoulders Pattern. A reversal pattern noted for its three points (left shoulder, head, and right shoulder) as well as the neckline, this pattern can also signal a reversal from a downtrend to an uptrend when the pattern appears to be upside down. As shown in Figure 1, we believe we are close to completing an inverse Head and Shoulders Pattern on the yield of the 10-year Treasury. A weekly close above the neckline near 0.95% would signal confirmation and target a move to just above 1.3%. The range from 1.3% to 1.5% also marks significant resistance for yields, as it was support for nearly a decade before breaking down in February.

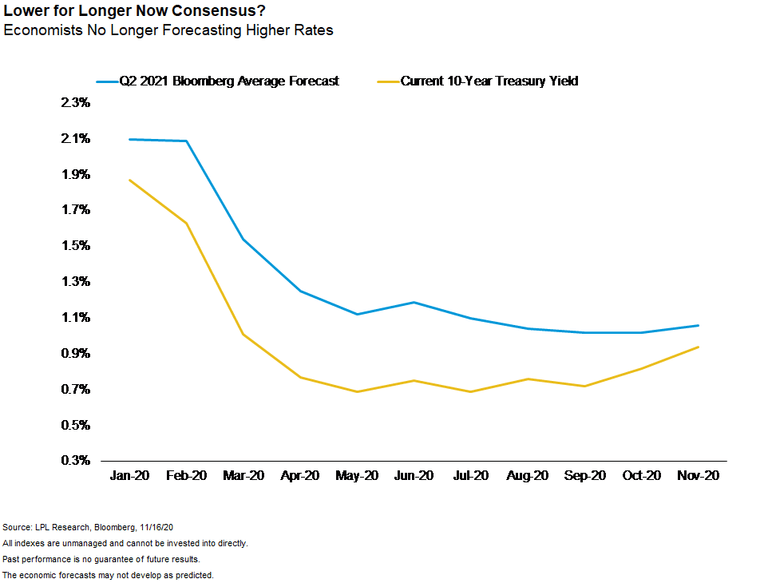

Lower for Longer Is Now Consensus

The fundamental arguments against higher rates are numerous. The economy is still recovering from a historic recession, COVID-19 cases are rising or hitting all-time highs in multiple regions of the country, and the Federal Reserve (Fed) has signaled it plans to keep short-term rates at zero for the foreseeable future. However, from a contrarian perspective, we believe there is a case to be made that “lower for longer” is now too consensus of a position, and that if the masses are already positioned for lower rates, those lower rates may be behind us. As shown in Figure 2, after consistently predicting higher interest rates throughout 2020 and revising forecasts lower as they fell, economists have been slow to revise forecasts higher even as yields have risen in recent months. In fact, the average forecast for the 10-year Treasury yield is now just 1.01% by the end of Q2 2021, implying barely a 10 basis point (.1%) move in rates over the next seven months.

According to LPL Financial Chief Market Strategist Ryan Detrick, “The consensus expectation is that lower rates are here to stay. But with a vaccine potentially on the horizon, and parts of the economy recovering faster than expected, the biggest risk for fixed income investors may be a sharp move higher in rates.”

As a reminder, bond prices move inversely to interest rates, and a move toward 1.3–1.5% in 2021, combined with the low absolute level of interest rates could mean near-zero returns for the Barclays Aggregate Bond Index in 2021. The poor near-term outlook for bond returns remains one of several key reasons we continue to favor stocks over bonds heading into next year.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from Bloomberg.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

{kind=link}

{kind=link}